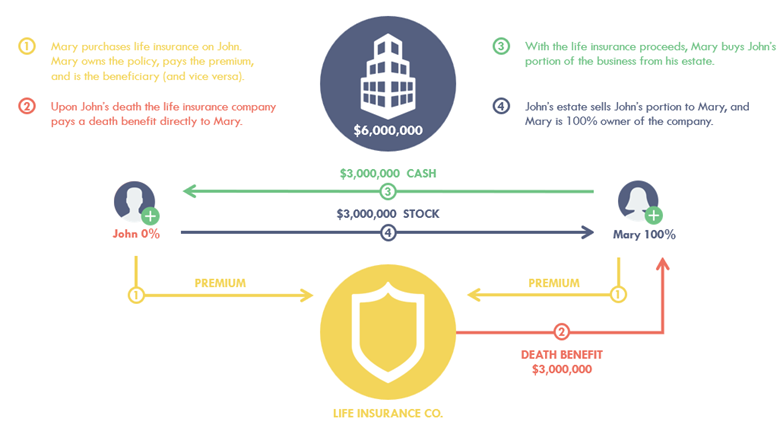

With two owners or members, a Cross-Purchase Agreement is a good solution. In fact, this is likely the agreement that should have been carried out in the first place. Most of the time, it’s ideal to write the check from the company, which is a valid reason for establishing an Entity Purchase Agreement.

Here, each owner or member would purchase life insurance on each other and own the policy, and the owners agree to buy and sell each other’s ownership interests.

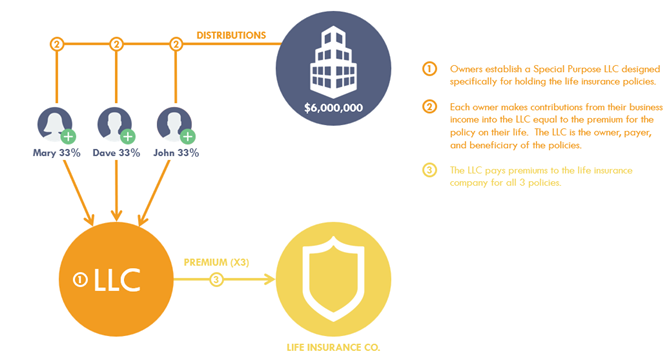

With more than two owners or members, it’s likely a Stock Redemption plan which makes the Special Purpose LLC a good choice for your business.

Here you would form another LLC with the same members or owners of the original business which buys life insurance on each of the members. An internal assignment of the contracts to avoid incidents of ownership by the insured on his or her own policy. If this isn’t done properly, the Connelly ruling may affect this agreement as well.

Remember that the best Buy-Sell structure for your business should align with your objectives, protect the interests of all owners, and provide a clear framework for handling ownership changes.